Financial advisors are closely tracking the benchmark 10-year Treasury note following the release of new inflation data on January 13, 2024. The Personal Consumption Expenditures (PCE) price index, which excludes food and energy, increased by 0.4% after a previous 0.2% gain in November, according to the Bureau of Economic Analysis. Year-over-year, core PCE inflation rose to 3.0% from 2.8% in November, surpassing Wall Street’s estimate of 0.3%. This data is significant as the U.S. Federal Reserve has set a 2% inflation target.

In response to the inflation figures, the 10-year Treasury yield increased by a basis point to 4.08%. This level is comparable to the yield back in September when the Federal Reserve began cutting interest rates. The slight rise in yield indicates that the Federal Reserve may maintain its current stance longer than anticipated, despite concerns surrounding rising employment levels.

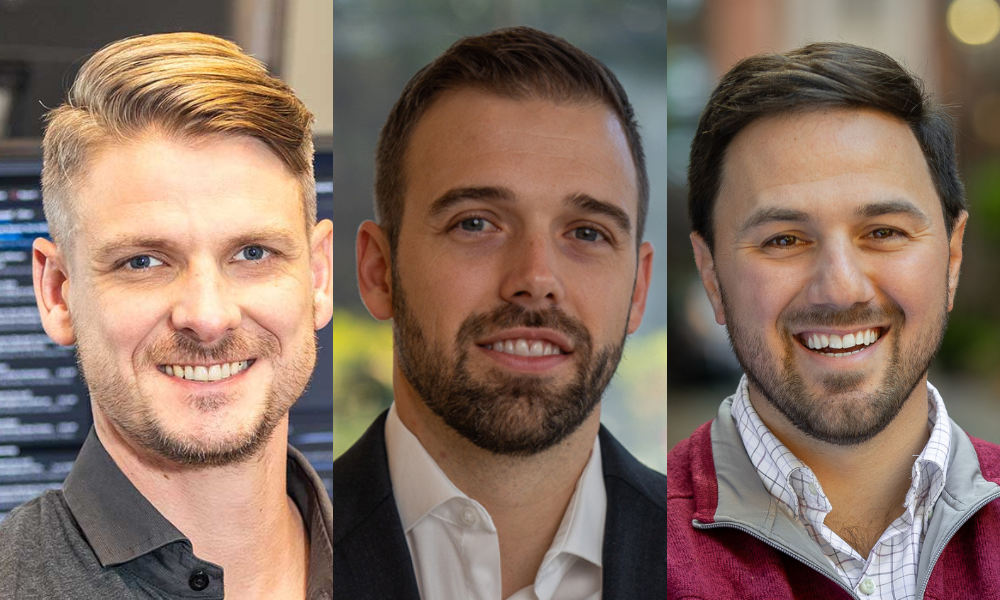

With the 10-year Treasury yield around 4%, Sam Diarbakerly, founder and private wealth advisor at Generation Capital Advisors, emphasizes a disciplined approach in managing fixed income. He advocates for a balanced barbell strategy, maintaining both short-duration and intermediate exposures without making extreme duration bets. Diarbakerly noted, “With yields near 4%, we are incrementally comfortable adding duration, but we are not making an aggressive directional call.”

Spencer Carlson, managing partner at Chappell Wealth Management, shares a similar perspective. He maintains a neutral duration stance, explaining that Treasuries serve a structural role in his portfolios rather than a tactical one. He stated, “Over long horizons, intermediate Treasuries have delivered positive real returns with materially lower volatility than equities.” Carlson believes that Treasuries are attractive diversifiers, especially given the unpredictable nature of short-term rate movements.

Mike Martin, vice president of market strategy at TradingBlock, is also adopting a neutral position for now. He indicated that if the 10-year yield approaches 4.5%, he may consider adding duration, pending inflation trends. He remarked, “Treasuries serve as downside protection,” particularly in light of current equity valuations and geopolitical uncertainties.

Outlook for Federal Reserve and Treasury Yields

Regarding the latest PCE reading, Diarbakerly asserts that his outlook is informed by broader trends rather than individual data points. He focuses on whether core PCE inflation continues to decline. “If core PCE confirms continued disinflation and the 10-year stabilizes or drifts lower, that supports maintaining our balanced barbell,” he explained. Conversely, if inflation accelerates again, he would consider adding selectively rather than withdrawing from the market.

For the first half of 2024, Diarbakerly anticipates that the Federal Reserve will remain cautious and data-dependent. He believes there is a high threshold for aggressive rate cuts unless labor markets significantly weaken. His strategy reflects a belief in a prolonged period of higher rates, gradual disinflation, and steady growth that is not recessionary.

Carlson echoes similar sentiments regarding the Federal Reserve’s dual mandate to balance inflation and labor market conditions. He points out that while inflation has notably decreased from its peak, it has not yet reached the target. “Given that backdrop, we expect continued caution from the Fed regarding rate cuts in spite of political pressures,” he said.

Both Diarbakerly and Carlson maintain that their bond allocations are independent of any near-term policy decisions. “Treasuries play a structural role in portfolios independent of whether rate cuts occur in the next few meetings,” Carlson added.

As the financial landscape continues to evolve, advisors are focusing on building resilient portfolios that can withstand various economic scenarios while capitalizing on opportunities for attractive income. The consensus among these financial professionals indicates a careful, balanced approach to navigating the complex interplay of inflation data and Treasury yields.