Stagnating economies and soaring government debt are pushing the United States, the United Kingdom, and European Union towards potential funding crises. As interest rates rise and growth lags, the risk of a debt trap is becoming increasingly evident. This situation raises the critical question: which region will be forced to seek external assistance first?

The Mechanics of a Debt Trap

Understanding the dynamics of debt is vital as the interplay between government borrowing and economic growth becomes more precarious. High levels of government debt, particularly in the Eurozone and the UK, are becoming unsustainable due to insufficient economic growth. In the United States, the situation is similarly concerning, with rising interest rates compounding existing debt burdens.

Historically, governments have managed to reduce debt-to-GDP ratios through significant economic growth. For instance, following World War II, the United States saw its debt-to-GDP ratio drop from a peak of 120% in 1946 to 35% by 1971. This was largely due to a robust increase in GDP, which grew by 483% during that period, while government debt increased by 142%. The increase in government revenues also outpaced the growth of debt, which played a crucial role in managing fiscal responsibility.

Today, however, the scenario is vastly different. As outlined by Alasdair Macleod in an analysis published by Von Greyerz, the rapid increase in government debt has not been matched by revenue growth. This disparity raises alarms, particularly as tax rates in many advanced economies are already high, limiting the potential for further revenue increases without deterring economic activity.

The Implications of Rising Interest Rates

The current economic environment is marked by rising interest rates, which are exacerbating the challenges faced by governments. A debt trap occurs when the growth rate of debt exceeds the growth rate of tax revenues. As borrowing costs increase, the sustainability of government finances comes into question. For example, the US Treasury is experiencing a classic debt trap, especially since the onset of the pandemic in 2020, with debt increasing at a much faster pace than revenue.

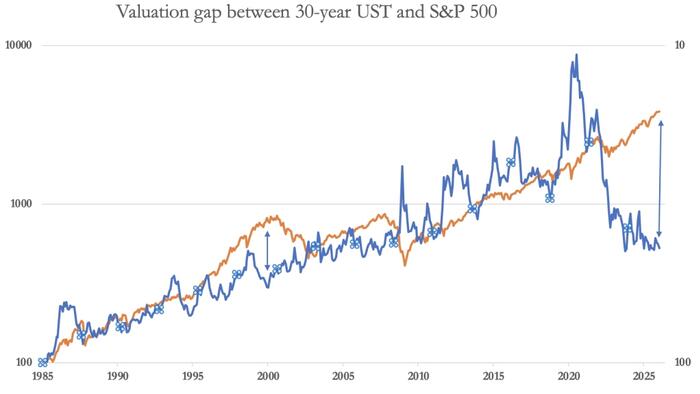

Interest rates have risen sharply between 2021 and 2023, challenging the US government’s ability to manage its debt. The Federal Reserve’s previous ability to suppress interest rates is diminishing, and foreign demand for US Treasury debt is declining, prompting a significant shift in how the Treasury finances its obligations.

Foreign investors, particularly in the BRICS nations and members of the Shanghai Cooperation Organisation, are increasingly moving away from the dollar, reflecting a broader loss of confidence in its stability. This shift is contributing to a funding crisis, as the US Treasury faces difficulties in attracting buyers for its long-term debt offerings.

The implications are profound. With a national debt now surpassing $38.6 trillion, the US government may need to rely more heavily on short-term borrowing, potentially leading to a further deterioration of its fiscal position.

As the risk of a debt crisis looms, the fundamental question remains: who will be forced to cut spending first? History suggests that market forces will ultimately dictate the course of action, and without proactive measures, a crisis may trigger necessary fiscal reforms.

This scenario serves as a stark reminder of the delicate balance between maintaining economic growth and managing government debt. As the situation develops, the potential for a significant economic adjustment grows, emphasizing the need for vigilance and strategic planning from policymakers across the globe.